Even if you secured a new mortgage recently, it might make sense to refinance. Prior to making the decision to refinance, take a look at these 5 home loan refinancing considerations.

1. Your Unique Needs

Your personal situation, needs, and goals are the foundation in your decision to refinance, and which loan program you should choose. Every mortgage and borrower varies, so an opportune situation for one homeowner may not be ideal for another.

Good reasons to refinance include:

- Lowering your interest rate to reduce your monthly payment

- Shortening the term of the mortgage to pay off your home or build equity faster

- Switching from an adjustable rate to a fixed-rate mortgage

- Getting cash for home improvements to increase your home’s value, while enjoying a nicer home

- Getting cash to consolidate consumer debt, substantially decreasing your total monthly debt payments

To illustrate how different needs affect whether refinancing makes sense for one person, but not another, consider the following scenarios:

Kathy and Greg purchased their home 10 years ago, and their third child is expected to be born within a few months. Although their total household income covers monthly expenses for now, that will completely change with the birth of their third child (increase in health insurance premium, food, diapers, clothing, and so forth). The couple considers refinancing back into a 30 year mortgage, despite having already paid 10 years into their current 30 year mortgage. The decision will save them several hundred dollars per month, which meets their unique need of having enough disposable income each month after the baby is born.

This might be an incredible option for Kathy and Greg, but not for Gina and Richard.

Gina and Richard purchased their home 10 years ago as well. Gina and Richard are close to retirement, and have done a great job of staying debt-free while saving for retirement. Both of them earn high salaries, and live very modest compared to their annual income. The couple realizes, when they retire, their pensions will only equal about one half of their current income. To offset such a drastic reduction in income, they plan to pay off their mortgage prior to retirement – eliminating a $2,000 mortgage payment. Refinancing into a 15 year mortgage ensures their mortgage plan is in-line with their retirement plan – which is their unique need.

You may have noticed that neither scenario mentioned interest rates. Why? Although getting a lower interest rate is important for any refinancing scenario, the homeowners’ unique needs are the primary factor when deciding what makes sense for them.

2. Interest Rates – The 1% Rule Misconception

You may have heard a friend, co-worker, accountant or even a financial planner say, “It only makes sense to refinance if you can reduce your interest rate by at least 1%.” This is one of the biggest misconceptions hurting homeowners today.

Depending on your existing mortgage amount, reducing your interest rate by .5% may yield a monthly savings that works for you.

Therefore, if you are only looking at the interest rate as a deciding factor, your monthly savings should be the focal point when making any final decisions. (Again, always determine if the benefit of the refinance meets your needs – rather than someone determining that for you).

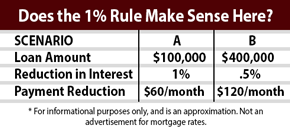

Consider Scenarios “A” and “B” to the right. You’ll notice someone with a $400,000 loan amount can achieve a $120 savings every month by reducing the interest rate by only .5%. However, someone with a $100,000 loan amount will save $60 each month if the interest rate was lowered by a full 1%.

As you can see, we can’t simplify the refinancing decision-making process by establishing a “1% Rule”.

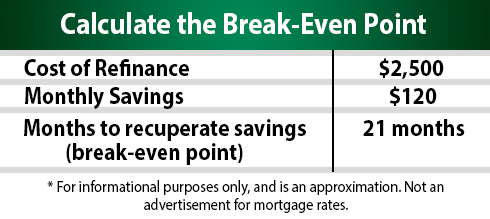

3. The Break-Even Point

Another consideration whether you should refinance an existing mortgage is the break-even point. This represents how long it will take you to recapture what is costs to refinance, through lowering your monthly payments. To calculate your break-even point, divide the expected cost of your refinance by the monthly savings of your new loan – resulting in the number of months it will take to recuperate the cost.

Although the break-even point is an easy calculation, there is no rule of thumb that makes sense for most borrowers. Some people feel keeping the break-even point under three years works well for them, while others say ten years. A good guide for you will be considering how many years you plan on owning your home. If you plan on selling your home within two years, and your break-even point is four years, then it may not make sense for you to refinance.

However, always consider if the monthly savings is crucial to your finances, despite knowing you may not recuperate the cost of refinancing.

In the event you receive a zero-cost refinance, your break-even point will be immediate – since there is no cost to refinance. In this scenario, lowering your interest rate by as little as an eighth of a percentage point may make sense.

4. Real Estate Market Value

You have likely heard the term loan-to-value. This ratio describes the amount of your loan against the property value. Because the real estate market continually fluctuates, so will the value of your home. Although a Realtor can prepare a general estimate of value, an appraisal is required to pinpoint the specific dollar value. Maximum loan-to-value ratios will apply (the exact percentage depends on the mortgage program). If the value of your property is less than the loan balance, you will have trouble refinancing unless you have funds to reduce the loan amount. Some loan options, such as an FHA streamline refinance, do not require an appraisal and thus make this less of an issue.

Approval Criteria

Every financing program has certain approval criteria that can affect if you qualify, and what interest you will receive. Below is a list of common factors you should be aware of:

- Loan-to-value Ratio

- Credit Rating

- Type of Property

- Dollar Amount of Loan

- Percentage Change in Monthly Payment

- Existence of Non-occupant Co-borrowers

- Mortgage Insurance Amount and Payment Period

CT Refinancing Considerations – The Next Step

As you can see from the 5 home loan refinancing considerations above, deciding to refinance includes more than comparing interest rates. It requires consideration of personal factors and evaluation of available options. An experienced mortgage professional will help you analyze these different pieces of information and help you make an informed decision. For additional CT refinancing considerations, contact a licensed loan officer at First World Mortgage.